Black Friday 3.52 Billion Thanksgiving 2.05 Billion 2017

The Friday after thanksgiving is called black Friday because that's when retailers finally turn profitable for the year. Not so much for market, however, because this morning it's red as far as the eye can see. The culprit: the same one we discussed late last night - the emergence of a new coronavirus strain detected in South Africa, known as B.1.1.529, which reportedly carries an "extremely high number" of mutations and is "clearly very different" from previous incarnations, which may drive further waves of disease by evading the body's defenses according to South African scientists, and soon, Anthony Fauci.

British authorities think it is the most significant variant to date and have hurried to impose travel restrictions on southern Africa, as did Japan, the Czech Republic and Italy on Friday. The European Union also said it aimed to halt air travel from the region.

"Markets have been quite complacent about the pandemic for a while, partly because economies have been able to withstand the impact of selective lockdown measures. But we can see from the new emergency brakes on air travel that there will be ramifications for the price of oil," said Chris Scicluna, head of economic research at Daiwa.

As a result, what was initially just a 1% drop in US index futures, has since escalated to a plunge of as much as 2% with eminis dropping the most since September, at one point dropping below 4,600 after closing on Wednesday above 4,700 as a post-Thanksgiving selloff spread across global markets amid mounting concerns the new B.1.1.529 coronavirus variant - which today will be officially called by the Greek lettter Nu - could derail the global economic recovery. Russell 2000 contracts sank as much as 5.4%. Technology shares may be caught in the net too as Nasdaq 100 futures slid.

The VIX increased as much as 9.4 vols to 28, it's biggest jump since January. It was last seen up 7.4 points, or the biggest increase since February.

Adding to the pain, there is nothing on today's macro calendar and the US market closes early which will reduce already dismal liquidity even more, exacerbating some of the moves throughout the session. Headlines are likely to center on various nations preventing travel from South Africa whilst potentially imposing more stringent COVID measures domestically, as well as which countries "find" the Nu variant.

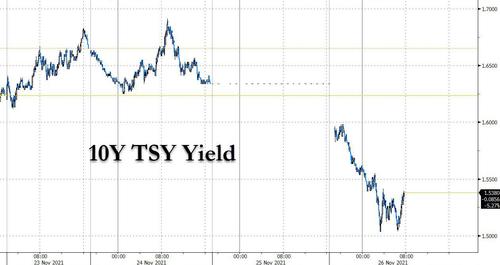

Amid the panicked flight to safety, 10Y TSY yields tumbled as traders slashed bets on monetary tightening by the Federal Reserve (just hours after Goldman predicted that the Fed would double the pace of its taper and hike 3 times in 2022, oops) ...

... as did oil amid fears new covid lockdowns will lead to a collapse in crude demand (they will also certainly force OPEC+ to put on pause their plans to keep hiking output by 400K every month).

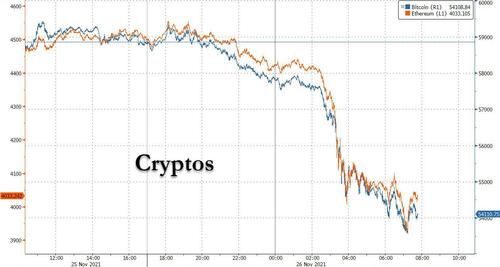

Paradoxically, even cryptos are tumbling, which is surprising since even the dumbest algos should realize by now that a new covid outbreak means more dovish central banks, no tightening, and if nothing else, more QE and more liquidity which is precisely what cryptos need to break out to new all time highs.

Cruise ship operator Carnival slumped 9.1% in premarket trading and Boeing slid 5.8% as travel companies tumbled worldwide. Stay-at-home stocks such as Zoom Video rallied. Didi Global shares fell after Chinese regulators reportedly asked the ride-hailing giant to delist from U.S. bourses. Here are some of the other big premarket movers:

- Airlines and other travel stocks slumped in premarket trading on growing concern about a new Covid-19 variant identified in southern Africa. The European Union is proposing to halt air travel from several countries in the area and the U.K. will temporarily ban flights from the region.

- United Airlines (UAL US) fell 8.9%, Delta Air (DAL US) -7.9%, American Airlines (AAL US) -6.7%; cruiseline-operator Carnival (CCL US) -12%; hotelier Marriott (MAR US) -6.1%; lodging company Airbnb (ABNB US) -6.9%.

- Stay-at-home stocks that benefit from higher demand in lockdowns rose in premarket, with Zoom Video (ZM US) gaining 8.5% and fitness equipment group Peloton (PTON US) +4.7%.

- Vaccine stocks surged in premarket, while Pfizer and BioNTech got an added boost after their coronavirus shot won European Union backing for expanded use in children. Moderna (MRNA US) rose 8.8%, Novavax (NVAX US) +6.2%, Pfizer (PFE US) +5.1%, BioNTech (BNTX US) +6.4%.

- Small biotech stocks gained in premarket as investors sought havens. Ocugen (OCGN US) added 22%, Vir Biotechnology (VIR US) +7.8%, Sorrento Therapeutics (SRNE US) +5%.

- Cryptocurrency-exposed stocks fell as Bitcoin dropped as investors dumped risk assets. Marathon Digital (MARA US) declined 9%, Riot Blockchain (RIOT US) -8.8%, Coinbase (COIN US) -4.6%.

- Didi Global (DIDI US) declined 6% in premarket after Chinese regulators were said to have asked the ride-hailing giant to delist from U.S. bourses.

- Selecta Biosciences (SELB US) dropped 13% in Wednesday's postmarket ahead of Thursday's Thanksgiving closure, after saying the U.S. FDA placed a clinical hold on a trial.

- Quotient Technology (QUOT US) gained 3.9% in Wednesday's postmarket on news that a board member bought $150,000 of shares.

What happens next will matter and so, all eyes are on the opening bell for the U.S. markets, set to return from the holiday for a shortened trading session. Tumbling futures and a soaring VIX signaled that the rout in Asia and Europe won't spare New York equities, while lack of liquidity will only make the pain worse. The Japanese yen emerged as the main haven currency of the day, with the dollar languishing.

"Every trader in New York will be rushing to the office now," said Salm-Salm & Partner portfolio manager Frederik Hildner, adding that news of the new variant could mean the end of the inflation and tapering debate.

The worsening pandemic poses a dilemma for central banks that are preparing to tighten monetary policy to curb elevated price pressures, according to Ipek Ozkardeskaya, senior analyst at Swissquote.

"It's terrible news,"Ipek Ozkardeskaya, a senior analyst at Swissquote, said in emailed comments. "The new Covid variant could hit the economic recovery, but this time, the central banks won't have enough margin to act. They can't fight inflation and boost growth at the same time. They have to choose."

"We now have a new Covid variant that's 'very' different from the ones we knew so far, a rising inflation, and a market bubble," she said. "The only encouraging news is the easing oil prices, which could tame the inflationary pressures and give more time to the central banks before pulling back support."

In the meantime, the World Health Organization and scientists in South Africa were said to be working "at lightning speed" to ascertain how quickly the B.1.1.529 variant can spread and whether it's resistant to vaccines. The new threat adds to the wall of worry investors are already contending with in the form of elevated inflation, monetary tightening and slowing growth.

In Europe, the Stoxx 600 index headed for the biggest drop in 13 months plunging 2.7%; travel and banking industries led the Stoxx Europe 600 Index down as much as 3.7%, the biggest intraday drop since June 2020. Airbus slumped 8.6% in Paris and British Airways owner IAG tumbled 12% in London, while food-delivery stocks gained. Here are some of the biggest European movers today:

- Stay-at-home stocks and Covid testing firms such as TeamViewer and DiaSorin are among the biggest gainers as worries over a new Covid variant send the Stoxx 600 tumbling on lockdown fears

- TeamViewer and DiaSorin rise as much as 6% and 7%, respectively

- On the down side, travel and leisure stocks plunge, with the likes of IAG, Lufthansa and Carnival posting double- digit falls

- IAG drops as much as 21%

- Software AG shares rise as much as 9.5% after Bloomberg reported that the firm is exploring strategic options, including a potential sale, with Morgan Stanley saying the company's biggest headwinds are behind it.

- Evolution gains as much as 4.6%, recouping part of Thursday's 16% plunge, with Bank of America saying the share price's "crazy time" amounts to a good buying opportunity.

- Skistar rises as much as 3.7%, bucking steep declines for travel and leisure stocks, after Handelsbanken upgraded the stock, saying bookings for the Scandinavian ski resort operator are "set to surge."

- Telecom Italia climbs as much as 2.8% following a Bloomberg report that private equity firms KKR and CVC are considering teaming up on a bid for the company.

- ING Groep falls as much as 11% after Goldman Sachs analyst Jean-Francois Neuez cut his recommendation to neutral from buy.

- Getlink drops as much as 6% as French fishermen start protests aimed at stepping up pressure on the U.K. in a post-Brexit fishing dispute.

Earlier in the session, MSCI's index of Asian shares outside Japan fell 2.2%, its sharpest drop since August. Casino and beverage shares were hammered in Hong Kong, while travel stocks dropped in Sydney and Tokyo. Japan's Nikkei skidded 2.5% and S&P 500 futures were last down 1.8%.

Giles Coghlan, chief currency analyst at HYCM, a brokerage, said the closure of the U.S. market for the Thanksgiving holiday on Thursday had exacerbated moves. "We need to see how transmissible this variant is, is it able to evade the vaccines - this is crucial," Coghlan said. "I expect this story to drag on for a few days until scientists have a better understanding of it."

Indian stocks plunged as the detection of a new coronavirus strain rattled investor sentiment globally, raising concerns over a likely setback to the nascent economic recovery. The S&P BSE Sensex lost 2.9%, the most since mid-April, to 57,107.15 in Mumbai, taking its loss this week to 4.2%, the biggest weekly drop since January. The NSE Nifty 50 Index declined by a similar magnitude on Friday. Reliance Industries was the biggest drag on both measures and declined 3.2%. "There is fear of this new variant spreading to other countries which might again derail the global economy," said Hemang Jani, head of equity strategy at Motilal Oswal Financial Services Ltd. Of the 30 shares in the Sensex index, 26 fell and 4 gained. All but one of 19 sub-indexes compiled by BSE Ltd. retreated, led by a index of realty companies. The S&P BSE Healthcare index was the only sub-index to gain, surging 1.2%. While researchers are yet to determine whether the new virus variant is more transmissible or lethal than previous ones, authorities around the world have been quick to act. The European Union, U.K., Israel, and Singapore placed emergency curbs on passengers from South Africa and the surrounding region.

Travel stocks were among the hardest hit. InterGlobe Aviation Ltd. fell 8.9%, Spicejet Ltd. slipped 6.7% and Indian Hotels Co. Ltd. plunged 11.2%, the most since March 2020. "Nervousness on the new variant of coronavirus and expectations of the U.S. Fed increasing the pace of tapering have led to recent market weakness," Amit Gupta, fund manager for portfolio management services at ICICI Securities Ltd. said. "This trend may take some time to recover as the WHO meeting on the new mutant variant impact and hospitalization rates in US and Europe will be watched by the market very closely."

Crude oil to emerging markets completed this picture of mayhem.

In rates, fixed income was firmly bid as Treasuries extended their advance led by the belly of the curve, outperforming bunds, while money markets pared rate-hike bets amid fears that a new coronavirus strain may spread globally, slowing economic growth. Cash Treasuries outperformed, richening 12-14bps across the short end, with Thursday's closure exacerbating the optics. As shown above, 10Y Treasury yields shed as much as 10 basis points while the Japanese yen jumped the most since investors' March 2020 rush for safety. Yields across the curve are lower by more than 8bp at long end, 13bp-15bp out to the 7-year point, moves that if sustained would be the largest since at least March 2020 and in some cases since 2009. Short-term interest rate futures downgraded the odds of Fed rate increases. Gilts richened 10-11bps across the curve, outperforming bunds by 4-5bps. Peripheral and semi-core spreads widen. In FX, JPY and CHF top the G-10 scoreboard with havens typically bid.

In FX, the Bloomberg Dollar Spot Index was little changed after earlier touching a fresh cycle high, and the greenback was mixed versus its Group-of-10 peers as the yen and the Swiss franc led gains while the Canadian dollar and Norwegian krone were the worst performers as commodity prices plunged. Traders pushed back the timing of a 25-basis-point rate increase by the Federal Reserve to July from June, with only one further hike expected for the remainder of 2022. It's a similar story in the U.K. where the Bank of England is now expected to tighten policy in February instead of next month. Wagers that the ECB will raise its deposit rate by the end of next year have also been slashed, with only a six basis-point increase priced in, half of that seen earlier this week. The European Union is proposing to follow the U.K. in halting air travel from southern Africa after the new Covid-19 variant was identified there. The yen is at the epicenter of skyrocketing currency volatility as the new virus variant shakes markets. The cost of hedging against swings in the Japanese currency over the next week, which captures the release of the next U.S. payrolls report, is the most expensive in more than a year.

In commodities, crude futures are hit hard. WTI drops over 7% before finding support near $73, Brent drops over 5% before recovering near $78. Spot gold grinds higher, adding $21 to trade near $1,809/oz. Base metals are sharply offered with much of the complex off as much as 3%.

Looking at the otherwise quiet day ahead, data releases include French and Italian consumer confidence for November, as well as the Euro Area M3 money supply for October. Otherwise, central bank speakers include ECB President Lagarde, Vice President de Guindos, and the ECB's Visco, Schnabel, Centeno, Panetta and Lane, and BoE chief economist Pill.

Market Snapshot

- S&P 500 futures down 1.9% to 4,607.50

- STOXX Europe 600 down 2.8% to 468.04

- MXAP down 1.8% to 193.33

- MXAPJ down 2.2% to 628.97

- Nikkei down 2.5% to 28,751.62

- Topix down 2.0% to 1,984.98

- Hang Seng Index down 2.7% to 24,080.52

- Shanghai Composite down 0.6% to 3,564.09

- Sensex down 2.7% to 57,234.83

- Australia S&P/ASX 200 down 1.7% to 7,279.35

- Kospi down 1.5% to 2,936.44

- Brent Futures down 5.8% to $77.46/bbl

- Gold spot up 0.9% to $1,805.13

- U.S. Dollar Index down 0.33% to 96.46

- German 10Y yield little changed at -0.31%

- Euro up 0.4% to $1.1259

Top Overnight News from Bloomberg

- The European Union is proposing to halt air travel from southern Africa over growing concern about a new Covid-19 variant that's spreading there, as the U.K. said it will also temporarily ban flights from the region

- Those close to the Kremlin say the Russian president doesn't want to start another war in Ukraine. Still, he must show he's ready to fight if necessary in order to stop what he sees as an existential security threat: the creeping expansion of the North Atlantic Treaty Organization in a country that for centuries had been part of Russia

- Bitcoin tumbled 20% from record highs notched earlier this month as a new variant of the coronavirus spurred traders to dump risk assets across the globe

- Germany's Greens tapped their two co- leaders to run the foreign ministry and take charge of an influential portfolio overseeing economy and climate protection in the country's next government under Social Democrat Olaf Scholz

A more detailed breakdown of global markets courtesy of Newsquawk

Asian equity markets declined and US equity futures were also on the backfoot on reopen from the prior day's Thanksgiving lull with markets spooked by new COVID variant concerns related to the B.1.1.529 variant in South Africa that was first detected in Botswana. The new variant showed a high number of mutations and was said to be the most evolved strain ever which spurred fears it could be worse than Delta and is prompting both the UK and Israel to halt flights from several African nations. ASX 200 (-1.7%) was negative with heavy losses in energy and broad underperformance in cyclicals leading the downturn across all sectors, while the much better than expected Australian Retail Sales data was largely ignored. Nikkei 225 (-2.5%) underperformed and gave up the 29k status as selling was exacerbated by detrimental currency inflows and with SoftBank shares among the worst hit on reports that China is said to have asked Didi to delist from US exchanges on security fears, which doesn't bode well for SoftBank given that its Vision Fund is the top shareholder in the Chinese ride hailing group with a stake of more than 20%. Hang Seng (-2.5%) and Shanghai Comp. (-0.7%) conformed to the risk aversion with the mood not helped by ongoing geopolitical concerns after a Chinese Defense Ministry spokesperson noted they are ready to crush Taiwan independence bid "at any time", while China also said it opposes US sanctions on its companies and will take all necessary measures to firmly defend the rights of Chinese companies. Beijing interference further contributed to the headwinds amid the request by China for Didi to delist from US which reports stated regulators could backtrack on and with Tencent subdued after some Chinese state-run companies restricted the use of Tencent's messaging app.

Top Asian News

- Stocks in Asia Set for Worst Day Since March on Virus Woes

- Mizuho CEO Steps Down After Regulator Hit on System Issues

- Meituan 3Q Revenue Meets Estimates

- Japan's Kishida Delivers $316 billion Extra Budget for Recovery

European equities are trading markedly lower (Stoxx 600 -2.9%) with losses in the Stoxx 600 extending to 3.8% WTD. Sentiment throughout the week has been hampered by various lockdown measures imposed across the region with the latest leg lower accelerated by new COVID variant concerns related to the B.1.1.529 variant in South Africa. The new variant has shown a high number of mutations and is said to be the most evolved strain so far. This has spurred fears it could be worse than Delta and has prompted multiple nations to halt flights from several African nations.The handover from the overnight session was an equally downbeat one with the Nikkei 225 (-2.5%) dealt a hammer blow by the risk environment and unfavourable currency flows. Stateside, futures are lower across the board with the RTY the clear laggard with losses of 4.2% compared to the ES -1.8%, whilst the tech-heavy NQ is faring better than peers but ultimately still lower on the session to the tune of 1.6%. Note, early closures in the US and subsequent liquidity conditions could exacerbate some of the moves throughout the session. With the macro calendar light, focus for the session is likely to centre on various nations preventing travel from South Africa whilst potentially imposing more stringent COVID measures domestically. Any further clarity on the spread of the variant and its potential to evade vaccines will be of great interest to the market and likely be the main driving force of price action today. Sectors in Europe are lower across the board with the Stoxx 600 Banking (-5.1%) sector bottom of the pile amid the declines seen in global bond yields as markets scale back expectations of central bank tightening (e.g. pricing now assigns a 63% chance of a 15bps hike by the BoE next month vs. 93% a week ago). Oil & Gas names (-4.8%) are suffering on account of the declines in the crude space with WTI crude in freefall with losses of 6.7% given the potential impact of travel restrictions on demand. Travel restrictions on South Africa (from UK, Israel, EU et al) and the potential for further announcements has crushed the Travel & Leisure sector (-5.7%) with airline names dealt a hammer blow; IAG (-13.5%), easyJet (-11%), Deutsche Lufthansa (-12%), Air France (-9.5%). Elsewhere, there are a whole raft of other laggards which are very much in-fitting with the March 2020 playbook but there are simply too many to list for the purpose of this report. Defensives and Tech are faring better than peers but ultimately still lower on the session to the tune of 1% and 1.9% respectively. Finally, for anyone wanting some positivity from today's session, the potential for further lockdowns has proved to be beneficial for the likes of HelloFresh (+3.2%), Ocado (+2.1%) and Delivery Hero (+1.9%).

Top European News

- Airlines Skid on South Africa Travel Bans Tied to Variant

- German Coalition Proposes a Combustion-Car Ban Without Saying So

- Putin Pushes Confrontation With NATO as Hardliners Prevail

- Siemens Is Said to Kick Off Sale of Postal Logistics Business

In FX, the index has been under pressure in the risk-averse environment amid a slump in yields and gains in its basket components – namely the JPY, CHF, EUR (see below) – and with liquidity also thinned by Thanksgiving. From a technical perspective, the index has declined from its 96.787 overnight high, through the 96.500 mark, to a low of 96.332 – with the weekly trough at 96.035. Ahead, the US calendar is once again light, with the US also poised for an early Thanksgiving closure; thus, impulses will likely be derived from the macro environment.

- JPY, CHF, EUR - Haven FX JPY and CHF are the clear outperformers as a function of risk-related inflows. USD/JPY has retreated from a 115.37 peak and fell through its 21 DMA (114.15) to a base around 113.66 - with the current weekly low around 113.64. USD/CHF retreated from 0.9360 to 0.9260 – with the 50 and 100 DMAs seen at 0.9234 and 0.9219, respectively, ahead of 0.9200. EUR/USD meanwhile gains on what is seemingly an unwind of the carry trade amid a spike in volatility. EUR/USD found support near 1.1200 before rebounding to a current 1.1288 peak.

- AUD, NZD, CAD, GBP - The non-US Dollar risk currencies bear the brunt of the latest market downturn, with losses across industrial commodities not helping. The Loonie has taken the spot as the biggest G10 loser as hefty COVID-induced losses in the oil complex keep the currency suppressed. USD/CAD trades towards the top of a current 1.2647-2774 range. AUD is also weighed on by softer base metal prices – AUD/USD fell from a 0.7200 overnight high to a current low at 0.7110. On that note, Westpac sees AUD/USD pushed down to 0.7000 by Jun 2022 (prev. 0.7700) amid rate differentials with the US; Westpac made significant changes to its FOMC policy forecast and now expect consecutive increases in the fed funds rate in Jun, Sept, and Dec 2022. NZD/USD is slightly more cushioned amid smaller exposure to commodities, and as the AUD/NZD cross takes aim at 1.0450 to the downside. GBP, meanwhile, was initially among the losers amid its high-beta status but thereafter nursed losses in a move that coincided with EUR/GBP rejecting an upside breach of its 21 DMA at 0.8475.

- EM - The ZAR is the standout laggard given the new South African COVID variant - B.1.1.529 COVID-19 variant (expected to be named Nu) – which is said to be the most evolved strain so far and thus prompted several countries to halt travel to the country of origin. USD/ZAR currently trades within a 15.9375-16.3630 intraday band. Meanwhile, the downturn oil sees USD/RUB north of 75.00 and closer to 76.00 from a 74.2690 base. The Lira also feels some contagion despite the lower oil prices (Turkey being a large net oil importer) – USD/TRY is back on a 12.00 handle and within 11.92-1226 parameters at the time of writing.

In commodities, the crude complex has been hit by compounding COVID fears which in turn triggered various travel restrictions and subsequently took its toll on global crude demand prospects. The new and more evolved South African variant prompted the UK, Singapore, and Israel to expand their travel red lists to include some African nations (Israel reported its first case of the new COVID-19 variant known as B.1.1.529). Japan also imposed tighter border restrictions. China's Shanghai city see flights impacted by its own outbreak. Europe also tackles its surge in daily cases - German Green Party's Baerbock (incoming Foreign Minister) does not rule out a German lockdown, according to Spiegel. EU Commission President von der Leyen is also to propose activation of the emergency air brake, to halt travel from southern Africa due to the B.1.1.529 COVID-19 variant. Losses in oil have exacerbated - with WTI Jan and Brent Feb now under USD 74/bbl (vs high 78.65/bbl) and USD 77/bbl (vs high 80.42/bbl), -6.0% and -5.0% respectively. This comes ahead of the OPEC+ confab next week, whereby OPEC watchers have suggested that oil prices will be a large contributor to the final decision. It is difficult to see how OPEC+ will increase output to the levels the US et al. will be content with, with the latest COVID downturn building the case for a pause in planned output hikes. Elsewhere, haven demand sees spot gold extend on gains above USD 1,800/oz after topping the 100 DMA (1,792.95/oz), 200 DMA (1,791.38/oz), 50 DMA (1,790.13/oz) overnight. Base metals are softer across the board amid the risk aversion. LME copper posts losses of around 3% at the time of writing, as prices threaten a more convincing downside breach of USD 9,500/t.

US Event Calendar

- Nothing major scheduled

DB's Jim Reid concludes the overnight wrap

Things have escalated on the covid front quite rapidly over the last 12 hours. Yesterday new covid variant B.1.1.529 was slowly starting to gather increasing attention but overnight it has begun to dominate markets and has caused a notable flight to quality with 10 year USTs -8bps lower. It was originally identified in Botswana and is starting to spread rapidly in Africa. The South African Health Minister has said it is "of serious concern". Almost 100 cases have already been identified in South Africa and the UK moved to put the country back (along with 5 other African nations) on a reinstated red travel list last night with others following this morning. The variant is said to be the most heavily mutated version yet and the WHO will meet today to decide if it is a variant of interest or a variant of concern. So a lot of eyes will be on how severe it is and whether it completely evades vaccines. At this stage very little is known. Mutations are often less severe so we shouldn't jump to conclusions but there is clearly a lot of concern about this one. Also South Africa is one of the world leaders in sequencing so we are more likely to see this sort of news originate from there than many countries. Suffice to say at this stage no one in markets will have any idea which way this will go.

Overnight in Asia all benchmarks are trading lower on the news with the Shanghai Composite (-0.50%), CSI (-0.64%), KOSPI (-1.27%), Hang Seng (-2.13%) and the Nikkei (-2.90%) all lower. Airlines and other travel stocks have obviously fallen heavily. Hong Kong has detected two confirmed cases of the new variant just as Hong Kong and China were considering quarantine-free travel. S&P 500 (-0.93%) and DAX (-1.82%) futures are also much weaker. Elsewhere, in Japan, CPI rose +0.5% year-on-year (+0.4% consensus and +0.1% previously), on the back of 16-month high fuel prices.

With the US out on holiday for Thanksgiving, there wasn't much going on yesterday after a very quiet day in markets. The variant news was only slowly creeping into the news flow so it hardly impacted trading. But in keeping with the theme of recent days, both inflation and the latest covid wave in Europe remained very much in the picture as jitters continue to increase that we could see further lockdowns as we move towards Christmas.

Starting with the headline moves, European equities did actually show signs of stabilising yesterday, with the STOXX 600 up +0.42% thanks to a broad-based advance across the continent. In fact that's actually the index's best daily performance in over three weeks, although that's not reflecting any particular strength, but instead the fact the index inched steadily but persistently towards a record high before selling off again a week ago. Other indices moved higher across the continent too, with the FTSE 100 (+0.33%), the CAC 40 (+0.48%) and the DAX (+0.25%) all posting similar advances. These will all likely reverse this morning.

One piece of news we did get came from the ECB, who released the account of their monetary policy meeting for October. Something the minutes stressed was the importance that the Governing Council maintain optionality in their policy settings, with one part acknowledging the growing upside risks to inflation, but also saying "it was deemed important for the Governing Council to avoid an overreaction as well as unwarranted inaction, and to keep sufficient optionality in calibrating its monetary policy measures to address all inflation scenarios that might unfold."

Against this backdrop, 10yr bond yields moved lower across multiple countries, with those on bunds (-2.3ps), OATs (-2.3bps) and BTPs (-1.9bps) all declining. There was also a flattening in all 3 yield curves as well, with the 2s10s slope in Germany (-3.0bps), France (-3.7bps) and Italy (-2.8bps) shifting lower. And the moves also coincided with a continued widening in peripheral spreads, with both the Spanish and the Greek spreads over 10yr bund yields widening to their biggest levels in over a year.

Of course, one of the biggest concerns in Europe right now remains the pandemic, and yesterday saw a number of fresh measures announced as policymakers seek to get a grip on the latest wave. In France, health minister Veran announced various measures, including the expansion of the booster rollout to all adults, and a reduction in the length of time between the initial vaccination and the booster shot to 5 months from 6. Meanwhile in the Czech Republic, the government declared a state of emergency and approved tighter social distancing measures, including the closure of restaurants and bars at 10pm. And in Finland, the government have said that bars and restaurants not using Covid certificates will not be able to serve alcohol after 5pm. All this came as the European Medicines Agency recommended that the Pfizer vaccine be approved for children aged 5-11, which follows the decision to approve the vaccine in the US. Their recommendation will now go to the European Commission for a final decision.

There wasn't much in the way of data at all yesterday, though German GDP growth in Q3 was revised down to show a +1.7% expansion (vs. +1.8% previous estimate). Looking at the details, private consumption was the only driver of growth (+6.2%), with government consumption (-2.2%), machinery and equipment (-3.7%) and construction (-2.3%) all declining over the quarter.

To the day ahead now, and data releases include French and Italian consumer confidence for November, as well as the Euro Area M3 money supply for October. Otherwise, central bank speakers include ECB President Lagarde, Vice President de Guindos, and the ECB's Visco, Schnabel, Centeno, Panetta and Lane, and BoE chief economist Pill.

Black Friday 3.52 Billion Thanksgiving 2.05 Billion 2017

Source: https://www.zerohedge.com/markets/black-friday-turns-red-terrible-news-global-markets-crater-nu-variant-panic